On Monday, September 23, package tour operator Thomas Cook PLC initiated compulsory liquidation proceedings after government, shareholders and lenders failed to agree on a rescue package.

The initial hope that the government counts a bailout of 150 million. ‘

The question of director incentives and moral hazard is fascinating. Moral hazard has always been an ambiguous concept that is interpreted on the one hand as a violation of responsible behavior of individuals and on the other hand, in more abstract economic terms, as an understandable and rational reaction to a subsidized price (often through state guarantees), implies morality does not play a role in these benefit-maximizing decisions .

Although Johnson’s reasons for his non-interference are the latter, his comments on the incentives for directors invite us to consider the former as well, the question not necessarily being whether Thomas Cook could have been saved, but whether it had to fail in a disorderly manner it did.

To answer this question, we need to examine two moral hazards: the compensation incentives that crowd out alternative strategies and benefit established management, and the treatment of goodwill, which means that failure is extreme and uncontrolled.

Despite running a company that struggled to break even as of 2010, Thomas Cook CEOs have been well rewarded: they have received over £ 35 million over the past 12 years. It would be unreasonable to assume that the company was run solely out of self-motivation, but it would also be naive to believe that the remuneration structures did not benefit them inappropriately despite the continuation of the company.

Understandably, no bonuses were paid in 2018, but in 2017 CEO Peter Fankhauser received 117% of his base salary as a bonus.

Thomas Cook CEO bonuses were paid according to five key performance indicators (KPIs): underlying net income (EBIT) (35%), group free cash flow (35%), net promoter score (15%), employee satisfaction (5%) and strategic progress on the new operating model (10%). But the devil is in the details, because the KPIs were based on non-standardized accounting figures.

The use and misuse of “underlying” figures in bonus calculations within the framework of a fair value regime has been dealt with elsewhere. Thomas Cook’s 2017 ‘underlying EBIT’ KPI calculation has crucially excluded exceptional items – and effectively removed £ 99m in exceptional costs from the bonus calculation.

This figure also virtually excludes financing costs, which in the case of Thomas Cook was high due to the company’s debt burden from previous mergers and acquisitions. Thus, the bonus was granted based on the “underlying EBIT” of £ 312 million rather than actual net income of £ 12 million.

In the case of debt-ridden acquisition companies with a lot of depreciating goodwill, it is unclear why CEO salaries are not valued after financing costs and depreciation. When excluded, CEOs have a strong incentive to pursue a debt-driven growth strategy in which the benefits of the newly purchased income streams are incorporated into the bonus payment, but the cost of loss is either excluded through the use of EBIT metrics or as ‘exceptional’ and is thus again excluded. This is ‘head I win, tails you lose’ management capitalism. It’s a moral hazard.

This type of compensation structure offers simple answers for managers looking to buy their way out of uncertainty. The lesson from Thomas Cook is that merging with or acquiring an affordable source of income “displaces” other more nuanced but difficult-to-implement restructuring strategies that require a rare level of management acumen to formulate the vision and execute the plan. This has a degenerative effect on the quality of British management: anyone can do it. It enables satisfactory behavior.

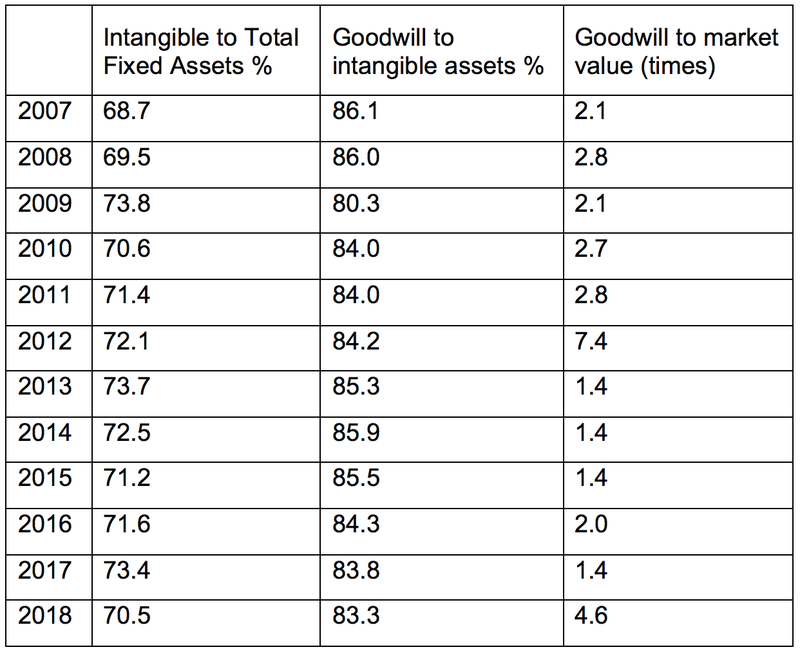

The second moral hazard is related to this. A key element in maintaining the company was the accounting treatment of the goodwill assets. Similar to other explosions like Carillion, Thomas Cook had intangible assets that made up around 70 percent of total reported assets, with goodwill making up about 85 percent of those intangible assets.

Goodwill was consistently two or more times the market value of the company for much of the period between 2007 and 2018, as shown in the table below.

Maintaining this goodwill assessment was of key importance to the stability of the company. The goodwill values should technically be the present value of the expected discounted future cash flows that flow into intangibles like brands, customer loyalty, etc. After changes to the accounting regulations in 2003 and 2004, goodwill is not amortized, but regularly subjected to an “impairment test” that reduces the value of the goodwill if these expectations are revised.

These impairment assessments are speculative in nature because they are based on estimates of events that have not yet occurred. In a context where impairments dampen profits and limit dividends, this could be read as a request to managers to maintain optimistic goodwill values for a longer period of time than can reasonably be justified on the basis of a particular performance history.

Between 2007 and the first half of 2019, Thomas Cook posted cumulative net profit losses of just under £ 2.8 billion, with 7 of those 13 periods being negative. This begs the question why the goodwill values have been kept at such a high level for so long. That’s enough time for expectations of the reality of a slowly declining company to normalize.

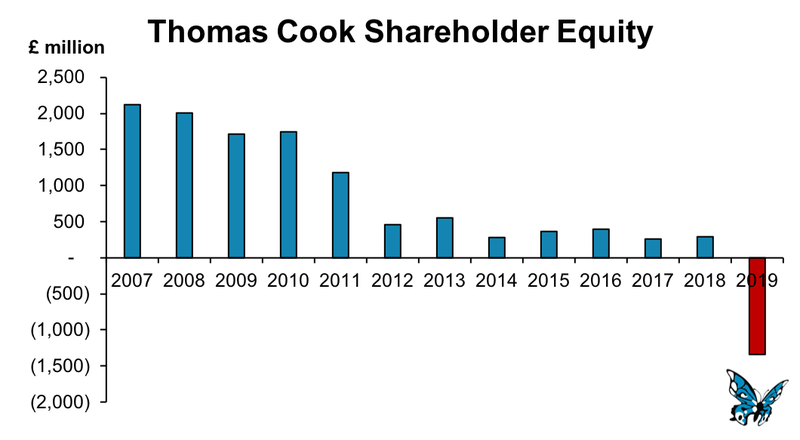

The longer the goodwill remains depreciated, the greater the depreciation on the day of settlement. In the first half of 2019, Thomas Cook finally had to write off £ 1.1 billion in goodwill, which tore a hole in the company’s balance sheet. The value of its intangible assets decreased from £ 3.06 billion in September 2018 to £ 1.96 billion in March 2019, effectively leaving the company with negative equity of £ 1.35 billion, as shown in the chart below. This is due to the double-counting effect (when you write off the asset you must make an equivalent write-down on the value of a liability, since both sides of the balance sheet must be “balance”).

This turned a company that could be shut down, dissolved or only modestly revived into a liquidation certainty. The company was kept alive by this flexibility in bookkeeping, which was management, but the most disorganized result for passengers, workers, suppliers, and the state.

There’s a strong argument that Thomas Cook’s goodwill should have been written off sooner as it would have allowed a softer landing for many stakeholders. Given its cost disadvantage over online sellers and the changing holiday habits of the UK public, it may not have been saved. However, his struggle for profitability was not aided by the interest burden on the debt incurred following the merger of MyTravel in 2007 and the merger of its retail activities with those of the Co-Operative Group and Midlands Co-operative Society in 2011, the it is even more difficult to generate positive net income from their operations.

There is therefore a generalizable risk that the Thomas Cook case illuminates – that we shall see something similar.Impairment shocks’ when the effects of the corporate debt bubble begin to resolve. Goodwill is the shadow asset of the corporate debt bubble. Cheap debt causes companies to pay many times their annual profit for their acquisition goals. This in turn leads to an increasing shift between market and book and consequently to a build-up of goodwill on company balance sheets.

This is paradoxical in this current phase of capitalism: high goodwill valuations should mean that expectations of future cash flows are also high; But these very high valuations of goodwill are now being booked at a time when long-term growth rates are low and the risks of global protectionism, trade wars, etc. are significant.

For acquiring companies with indebted balance sheets, this could become very chaotic if observers suddenly question the cash flow expectations on which their goodwill valuations are based.