With vaccination soaring in the developed world, it’s understandable that investors found tourism stocks pretty attractive before their sales and earnings numbers spiked.

In the meantime, the US Center for Disease Control and Prevention (CDC) has given cruise ships the go-ahead to stop operating some “Test drives”A Conditional Sailing Certificate from grid operators in US waters.

In the context of this impending rebound for one of the worst-hit segments of the travel and leisure industry during the pandemic, the following article is designed to provide insightful information on the top three cruise ship operators you could invest in, while also mentioning two non-traditional cruise ship stocks to consider if you want to get involved in this sector.

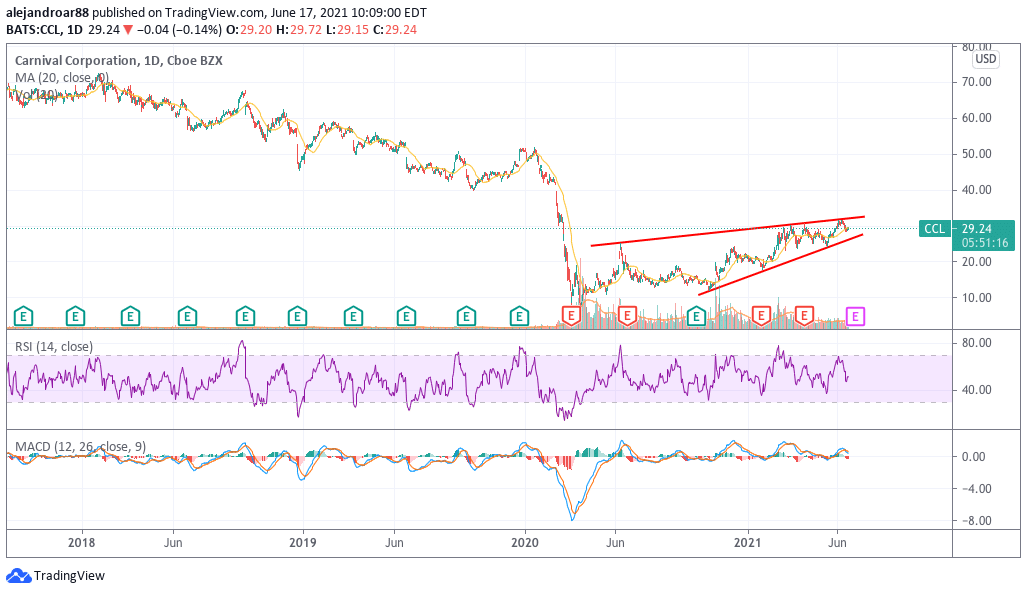

1. Carnival Corp (CCL)

This year, Carnival Corporation (CCL) stock has outperformed its two other publicly traded competitors, with the stock seeing a remarkable 36% gain since early 2021.

Before the pandemic, Carnival stocks were quite attractive as the company managed to triple its earnings from 2013 to 2019, with net earnings totaling $ 3 billion by the end of that year, with an average annual growth rate of 19% .

However, the virus crisis turned the tables for the cruise operator, forcing it to increase its long-term commitments from $ 9.7 billion to nearly $ 28 billion with around $ 57 billion in assets by the end of the first quarter of 2021 . It’s important to note that the book value of cruise line ships always makes up the bulk of their assets.

Meanwhile, Carnival’s sales continue to be pretty depressed as the company has not been able to fully resume operations.

For now, analysts are anticipating a full resumption of operations for the company by the third quarter of this year, with sales expected to hit $ 3.5 billion, while profitability is not expected to return to positive territory until the second quarter of 2022.

With a market cap of $ 32 billion, of which $ 11.5 billion is cash that may or may not be incinerated in subsequent quarters to fully resume operations, Carnival will be 7-10 times the Profit before the pandemic.

Even considering that interest expense is likely to gobble up a large chunk of Carnival’s profitability in the near future, current valuation still looks attractive if you are willing to hold the stocks for two to three years until the world does that again is what it was before the virus situation stopped.

67% of all retail investor accounts lose money when trading CFDs with this provider.

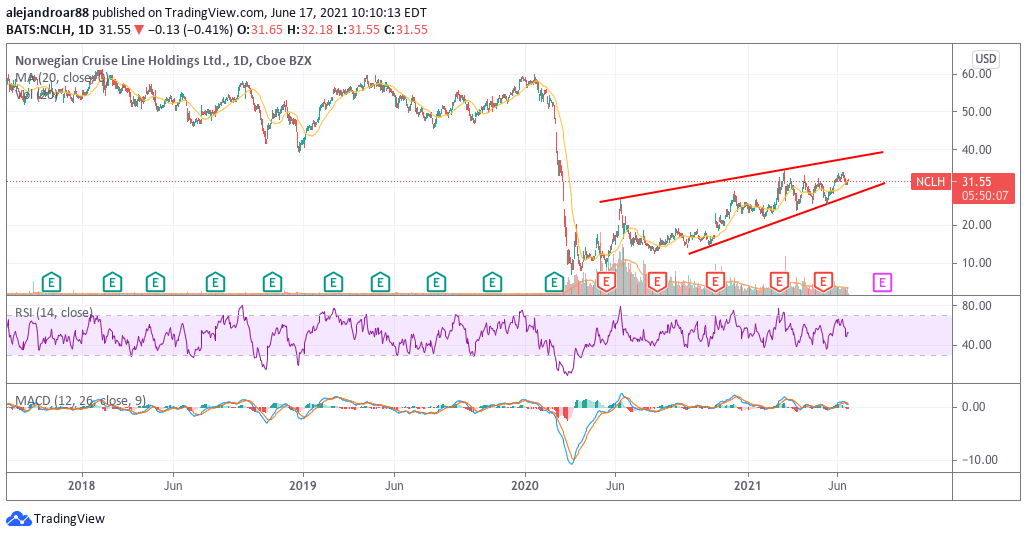

2. Norwegian Cruise Line Holdings (NCLH)

Norwegian Cruise Line Holdings (NCLH) is the second best performer to date among listed cruise line operators this year, bringing investors a solid 25.4% gain since the start of 2021.

Before the pandemic, the company had managed to double its net income nine times, from $ 103 million in 2013 to $ 930 million by the end of 2019, with a solid 44% cumulative annual growth rate.

The pandemic forced the company to borrow roughly $ 12.5 billion, with long-term commitments currently at $ 21.5 billion on assets of $ 34.35 billion. That slightly higher leverage ratio of 62.5% compared to Carnival’s 49% ratio is possibly why the company’s performance was lower than that of its competitors as the market is demanding a higher premium on the stock given the company’s increased solvency . Risk.

However, the stock trades at only 12 times 2019 annual earnings, and given the company’s impressive track record of earnings growth, I believe Norwegian could offer significant upside potential once it fully resumes operations.

67% of all retail investor accounts lose money when trading CFDs with this provider.

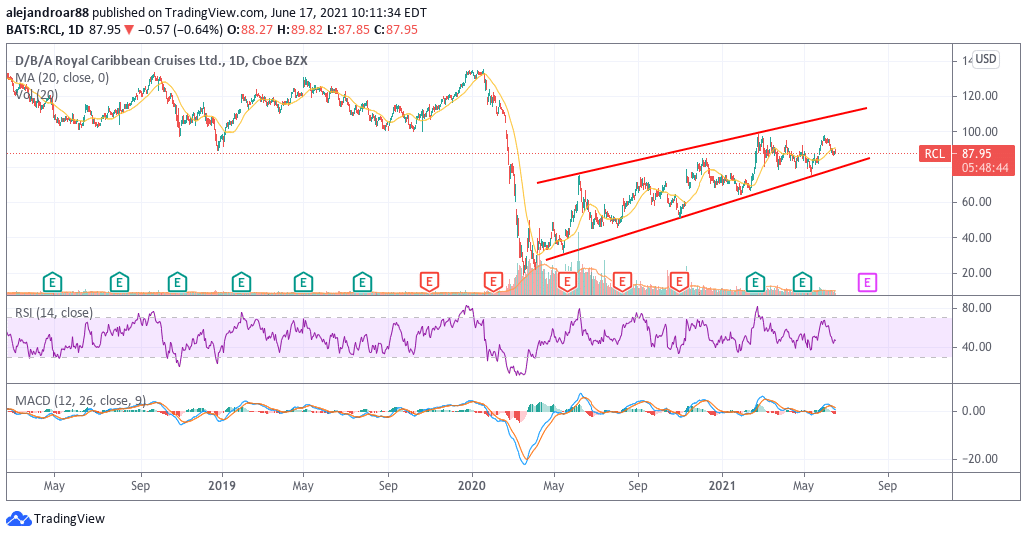

3. Royal Caribbean Group (RCL)

Royal Caribbean is lagging behind its two competitors this year as the stock has risen 18.5% so far in 2021 – nearly 17% less than the uptrend Carnival stock saw over the same period.

Before the pandemic, the company had an excellent track record of growing profitability. Net income rose from $ 474 million in 2013 to $ 1.9 billion by the end of 2019, with a solid cumulative annual growth rate of 26%.

Meanwhile, from a solvency perspective, the company had to borrow around $ 12.5 billion in debt to weather the health crisis, and that has raised its leverage ratio to 58%, making it the second-largest company in the group.

At its current market cap of $ 22.4 billion, the company is trading around 12 times its pre-2019 pandemic net income, and similar to its peers, that rating seems fair given the risks these companies are still facing .

67% of all retail investor accounts lose money when trading CFDs with this provider.

4. Disney (DIS)

Perhaps you are not as familiar with these two names as the three I listed above. However, Disney (DIS) is also a cruise company that owns four ships.

Before the pandemic, the company had planned to add three more ships to its cruise fleet, which should be delivered in 2021, 2022 and 2023, respectively. This division is part of Disney’s Parks, Experiences and Products division and contributed a portion of the company’s $ 26.22 billion in revenue through fiscal 2019.

67% of all retail investor accounts lose money when trading CFDs with this provider.

5. Saga Plc (SAGA)

Saga Plc (SAGA) is now a UK company providing tourism solutions in the UK. The company owns a small fleet of cruise lines that generated $ 96.6 million in 2019 revenue for the company, accounting for nearly 20% of Saga’s total travel revenue.

While these aren’t pure cruise operators, investors could view these companies as potential companies in the cruise industry, as a recovery in revenue from that particular segment of their business could boost their top-line results in the years to come.

67% of all retail investor accounts lose money when trading CFDs with this provider.