stock: 100% dilution hints at disappointment for investors")

[Author’s Note: CTRM executed a 1 for 10 reverse split on 5/28/21. All share and per share numbers in this article have been adjusted accordingly]

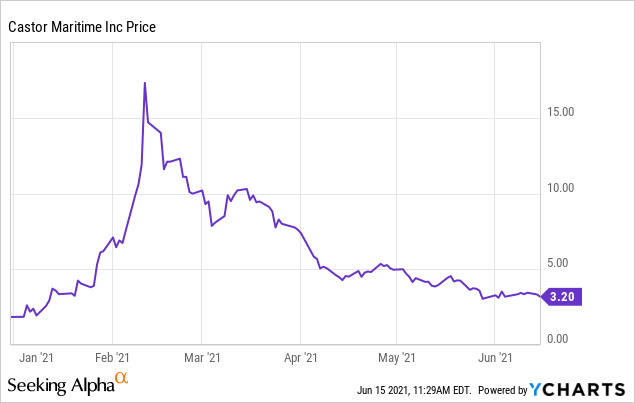

Castor Maritime (CTRM) is a Marshall Islands company controlled by an individual, Mr. Petros Panagiotidis, based in Cyprus. Readers who have read my previous articles on the company (here, here, here, and here) will know that CTRM has been a favorite of the Reddit (with two sub-Reddits here and here) and StockTwits crowds for the last several months . This sudden popularity has caused the stock price to fluctuate as can be seen in the year-to-date chart below.

New edition

Today (June 15), CTRM filed a prospectus supplement (which “brochure“), which will provide for the issuance of up to $300 million worth of common shares. The share price, as I write, is $3.14, suggesting an issuance of approximately 95.5 million common shares. Prior to this one new issue, CTRM had 89,995,848 shares outstanding, so this issue will likely result in more than doubling the number of common shares.To understand what this means for shareholders, I think it’s useful to look at two basic CTRM -View areas – CTRM’s stock history since listing and the alignment (or lack thereof) of management’s incentives with shareholder interests.

stock history

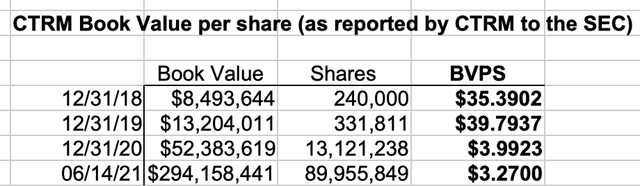

When CTRM listed on NASDAQ in February 2019, it had 240,000 shares outstanding. As of June 14, 2021, the number of shares outstanding had grown to approximately 89.5 million. This stock issuance explosion sheds light on the company’s fundamental business model. CTRM is constantly issuing shares to buy ships and grow the company. The problem for investors is that the pace of stock issuance has far outpaced asset growth. Since the listing, CTRM’s assets have grown by about 2,000% (from $10 million to $215 million), its fleet has grown 2,500% (from 1 ship to 26, on a fully delivered basis) but the number of shares has grown 3,700%. Of course, this has extremely destroyed the shareholder value. Book value per share is down more than 90% since the end of 2018:

(Source: CTRM filings, own calculations)

(Source: CTRM filings, own calculations)

Note that all share offerings except April 2021 have been at a discount to book value, taking value away from existing shareholders in favor of incoming shareholders, and the dilution announced today is likely to be the same.

The interests of the shareholders do not seem to be the priority. Why not? The answer lies, I believe, in the management incentive structure.

What drives the CEO?

Mr. Petros Panagiotidis is CEO, CFO and sole employee of CTRM. His legions of fans on Reddit and StockTwits refer to him simply as Petros (and so I take liberty to do the same).

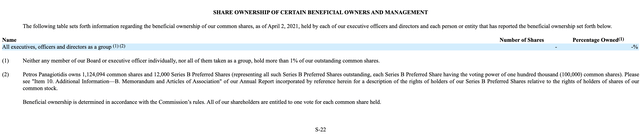

When CTRM went public in 2019, Petros owned 112,409 common shares — a little less than 47% of the company. When he last reported on April 2, 2021, he had the same 112,409 shares. As I’ll show in this section, that holding of less than $300,000 (and even the roughly $2.7 million unrealized loss he’s incurred over the past 2.5 years as a result) is in comparison to the other value it has withdrawn and will withdraw from its shareholders, insignificantly the same period.

The revenues that Petros (and when I speak of Petros I include the two Liberian companies through which he trades) derive almost entirely from the size of the fleet. Although he has a base fee of $1.2 million per year, the vast majority of his income comes from (i) his 1% fee on ship acquisitions, (ii) his 1% fee on disposals vessels, (iii) its 1.25% interest in all charter earnings and (iv) its fee of $250 per vessel per day. Whenever the company raises capital, be it equity or debt, and uses it to buy ships, Petros immediately earns 1% of the net amount raised. Looking at equity and debt raised to date ($51 million) and adding the equity of $300 million announced today, that translates to a total of $9.9 million in initial and acquisition fees over the years 2019 through 2021 , provided he does not raise any further debt or equity. When all funds are spent and all ships are operational, CTRM could have a fleet of 50 ships generating revenue of $400 million per year, which would generate about another $10 million per year in recurring fees (note Note that the 1.25% fee is based on gross receipts and not income).

Investors may wonder if these incentives (all of which are fully and properly disclosed in the Company’s filings, including on pages S-8 and S-9 of the Prospectus Supplement, as shown above) explain why the Company continues to expand its fleet , regardless of market conditions, and uses any cash flow for further acquisitions rather than returning cash to investors through dividends or buybacks. In fact, CTRM has never paid a dividend on its common stock and has never repurchased any stock.

Investors may wonder if these incentives (all of which are fully and properly disclosed in the Company’s filings, including on pages S-8 and S-9 of the Prospectus Supplement, as shown above) explain why the Company continues to expand its fleet , regardless of market conditions, and uses any cash flow for further acquisitions rather than returning cash to investors through dividends or buybacks. In fact, CTRM has never paid a dividend on its common stock and has never repurchased any stock.

Can the situation be changed?

Because Petros has such a small position in the common stock — less than 0.12% prior to today’s announcement and likely about half that after the reissue, CTRM investors may be wondering if shareholders are taunting the CEO and/or his incentives through shareholder action can change. Unfortunately, despite such a small stake, Petros has retained full control of the company. Specifically, he owns all of the shares of a special class of shares (the Series B Preferred Stock), which gives him 1.2 billion votes compared to the 89.5 million votes controlled by common shareholders. Even if today’s issue should lead to a doubling of the free float, he will still have a very comfortable majority.

Conclusion and Outlook

Conclusion and Outlook

When I first started following this company (woken up by an excellent analysis by SA contributor Henrik Alex) I thought this was a review story. As I discussed in my article “Castor Maritime: The CEO feeds the bears“, the stock price deviated so far from fundamentals that even the CEO felt compelled to point out the discrepancy in late March. I felt (and wrote) that the stock price was heading towards book value (or NAV, which is very strong). ) would fall similarly for this company which has acquired well over 90% of its tangible assets in the last 4 months.) However, as I delved deeper into the company and specifically into the management incentives, I changed my mind In this case I believe that the company’s fundamentals don’t matter because, in my view, management’s incentives are so misaligned with shareholders’ interests that shareholders will never share in the success of the underlying business. Dilution reinforces my view.

In the unlikely event that CTRM returns cash to shareholders, that the CEO relinquishes his absolute voting majority, or that regular dilutions cease (this is the sixth dilution in just over 12 months), I will change my mind. Until that happens, I advise all investors to avoid CTRM.