: More upside amid bright oil consumption outlook")

Typically, after an ETF is up over 150% in just 18 months, that would be reason for some profit-taking. However, the Energy Select Sector SPDR ETF (NYSEARCA:NYSEARCA:XLE) remains one of the few attractive areas in the US market. The ongoing rally Oil prices continue to lift earnings prospects, while the rally in US stocks means the energy sector accounts for a tiny fraction of the overall market. Especially in comparison to the market as a whole, the recovery in the energy sector is likely to have only just begun.

The XLE tracks the performance of the Energy Sector Select Index, which in turn tracks the S&P 500 components involved in the development or production of energy products. The ETF charges a minimal fee of 0.12%, which pales in comparison to its trailing dividend yield of 3.7%. While the index does not include a number of international oil majors such as BP (NYSE:BP) and Royal Dutch Shell (NYSE:RDS.A) (NYSE:RDS.B)which we also believe have upside potential, we already have exposure to these stocks via the EWU ETF (see “EMU: Remain bullish amid dividend recovery‘).

Upward momentum is building

The XLE closed yesterday at its highest level since January 24, 2020 after holding above near-term resistance-turned-support as illustrated in the chart below. The next significant upside target is around $65, where the downtrend line resistance cuts off the 2014 highs.

XLE stock price

Source: Bloomberg

The rally at WTI also looks healthy. The front month contract has breached the $70 level and the next upside target is the October 3, 2018 high of $76.90. In my view we are likely to get there soon as bullish momentum appears to be building after the successful hold above major long-term resistance-turned-support (see chart).

Front Month WTI price

Source: Bloomberg

The rebound in oil prices should herald a major turnaround for the XLE’s relative performance. The chart below shows the relationship of the XLE to the SPX, which seems to trace a large inverted head and shoulders pattern. A break above the neckline resistance would roughly double the XLE compared to the SPX.

XLE to SPX ratio

Source: Bloomberg

Source: Bloomberg

Forward looking valuations continue to slide on oil recovery

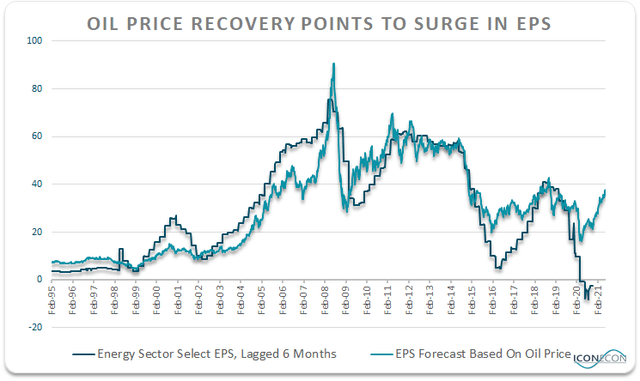

The ongoing recovery in oil prices continues to put downward pressure on the expected PE estimates for the XLE, with the recent reading coming in at 20.6x. However, this estimate likely does not take into account the further rally in oil prices that has taken place in recent weeks. The chart below shows the trailing gains of XLE’s underlying Energy Sector Select versus the 12-month forward WTI price, with gains lagging by 6 months. Based on historical correlation, earnings should reach $37 per share over the next 6 months, which would equate to a PE ratio of around 15x.

Source: Bloomberg, own calculations

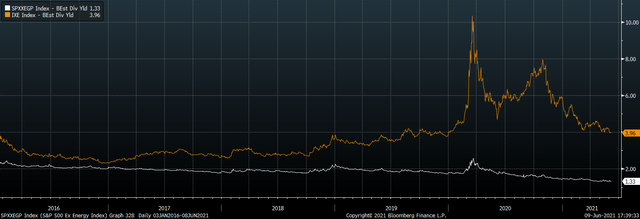

The free cash flow outlook is even more impressive, as the expected FCF yield is now 7.7%, thanks not only to the rise in oil prices but also to restructuring and prioritization efforts by oil companies. It therefore seems very likely that the attractive dividend yield of the Energy Sector Select will continue to rise without further price gains. With dividends expected to recover from their 2020 crash, the expected dividend yield currently stands at 4.0%, 3x higher than the SPX Ex-Energy Index.

Energy Sector Select Dividend Yield vs. SPX Ex-Energy Dividend Yield

Source: Bloomberg

As we have shown in previous articles on the XLE, the energy sector’s share of the S&P 500 market cap tends to track the inflation-adjusted oil price over time. The chart below, updating our regular weekly chart with daily data, shows that the XLE remains as cheap as ever in the context of record high SPX prices and the recovery in oil prices.

The future of oil consumption remains bright

One thing that struck me about the doom and gloom surrounding the oil price decline over the past few years was the extent to which analysts agreed on the so-called death of fossil fuels despite the lack of evidence to back it up. like me in ‘Oil Stocks: Highest Herd Mentality‘, the prevailing bearish wisdom regarding the oil market is the polar opposite of what was observed just over a decade ago when the peak in oil supply rather than the peak in oil demand was the dominant narrative.

Belief in the global economy’s ability to wean itself off fossil fuels remains largely unfounded in emerging markets, I believe, due to the vast infrastructure required to reduce the West’s oil consumption and the continued prioritization of economic growth over the environment.

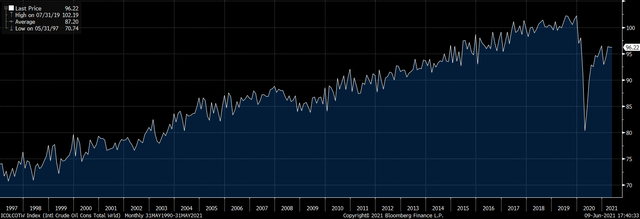

Additionally, there is now a growing body of research on the energy-intensive nature of electric vehicle production, which appears to be the mainstay for the peak oil demand theory. As is often the case, prices dictate the narrative, and the drop in oil prices since 2008 has bolstered the theory of peak oil demand, though largely driven by increased production from the US shale boom. Even with most of the world in some sort of Covid-related state of emergency, oil and liquid fuel consumption is just 6% below all-time highs, according to the US Energy Information Administration.

Global oil and liquid fuel consumption, millions of barrels per day

Source: Bloomberg, US Energy Information Administration.

If inflation continues to rise, oil stocks will outperform dramatically

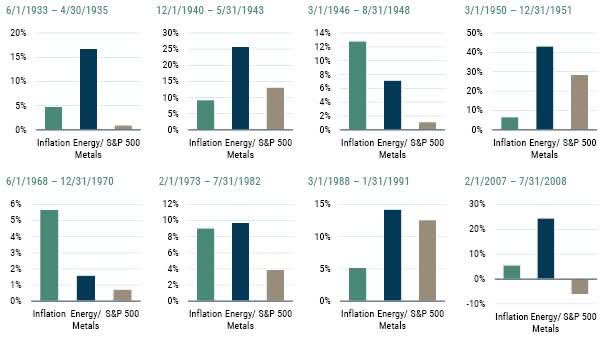

As we argued in XLE: 4 Reasons to Own Energy Stocks, energy stocks are very sensitive to inflation expectations because oil is relatively easy to store and demand is inelastic throughout the production process of almost all manufactured goods. A recent article by GMO concluded that commodity stocks in general tend to dramatically outperform the S&P 500 during periods of inflation, as illustrated in the chart below.

Performance of resource stocks during periods of inflation

Source: GMO

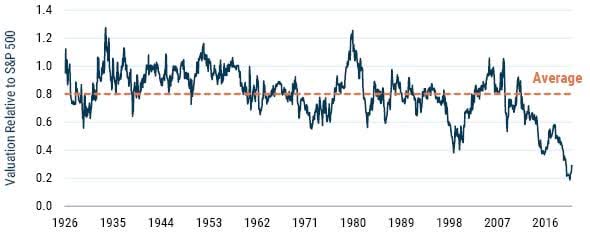

They also note that while their track record of inflation hedging would justify a valuation premium given the recent surge in inflation, commodity stock valuations are heavily discounted relative to the broader market.

Valuations of resource companies versus the S&P 500

As of 03/31/21 | Source: S&P, MSCI, Moody’s, GMO. The valuation metric is a combination of P/E (normalized historical earnings), price to book, and dividend yield.

summary

We have been heavily bullish on the XLE over the past year, and despite gains of over 150% from its lows, the ETF remains undervalued relative to oil prices and the broader market. The trailing dividend yield of 3.7% should rise in the absence of more XLE earnings as rising free cash flows allow dividend increases to resume. As for the long-term outlook for energy consumption, fears of a spike in oil demand appear to be completely overblown.