")

BCB Bancorp, Inc. (NASDAQ: NASDAQ:BCBP) is likely to benefit from the vaccine-driven economic recovery in New Jersey and New York. In addition, pension expenditure is likely to remain modest this year due to the already high level of reserves. In addition, there is scope for a decrease in custody costs. Overall, I expect the company to report earnings of $1.27 per share for the final three quarters of 2021, which will bring full-year earnings per share to $1.66, an increase of 47% compared to the previous year. The price target for December 2021 indicates a high upside potential compared to the current market price. In addition, BCB Bancorp offers an attractive dividend yield for a bank holding company. As a result, I am assuming a bullish rating on BCB Bancorp.

Recovery in regional markets to support credit growth

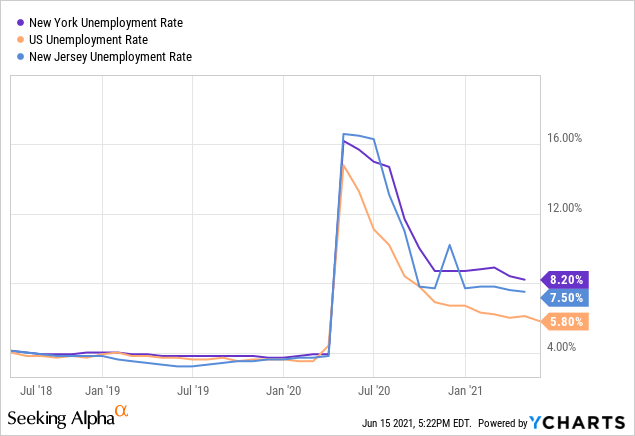

BCB Bancorp operates in New Jersey and New York. Unemployment rates in these two states are quite high compared to the rest of the country, as shown in the chart below.

However, the future looks brighter for these states because they have been at the forefront in dealing with the pandemic. According to the CDC, New York State excluding New York City had just 14.5 cases per 100,000 people over the past seven days, versus a national average of 26.2 cases. Additionally, New Jersey had just 18.9 cases, while New York City had 19.5 cases of COVID-19 per 100,000 residents over the past 7 days. As a result, I expect little credit growth in the coming year.

In my opinion, BCB Bancorp’s handling of the Paycheck Protection Program (“PPP”) is a cause for concern. The company referred its customers to The Loan Source, Inc., an SBA small business lending company, as mentioned in its first-quarter earnings release. I’m afraid this tactic may result in a loss of clients to other financial institutions.

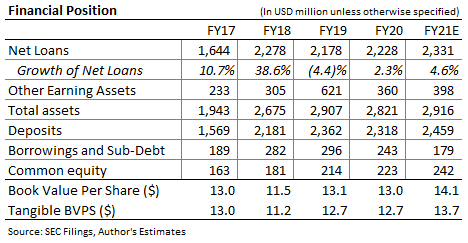

Overall, I expect the loan portfolio to increase by 1.5% by the end of December compared to the end of March 2021. Meanwhile, deposit growth should slightly outpace loan growth. Given the mismatch in deposit and loan growth, I expect lower-yielding assets to continue growing strongly in the coming year. The table below shows my balance sheet estimates.

Yield pressures are eroding the benefit of deposit repricing

BCB Bancorp has significantly reduced its deposit costs over the past few quarters. The cost of deposit still has room for further decline as the book of certificates of deposit (“CD”) is currently at a high rate. As reported in the Q1 10-Q filing, BCB Bancorp’s CD portfolio had an average balance of $683 million in Q1 2021, accounting for 28.4% of total loans.

The CD book had a high weighted average price of 1.17%. By my calculations, every 10 basis point decrease in the average CD cost can reduce the total cost of deposits by 3 basis points. In my opinion, BCB Bancorp can easily reduce its CD costs by 10 to 20 basis points this year given the low interest rate environment.

The pressure on the average portfolio return is likely to erode the benefit of CD repricing to net interest margin. BCB Bancorp focuses primarily on lending to the commercial and multi-family lending segments, and to the 1-4 family residential lending segments. These loan portfolios can have relatively long maturities. As a result, interest rate cuts have a delayed impact on the average portfolio return. The interest rate cuts of early 2020 are likely to put further pressure on portfolio returns in the coming year.

Overall, I expect the net interest margin to decline by eight basis points over the last three quarters of this year, compared to 3.48% in the first quarter of 2021. Pressure on the net interest margin will likely offset growth in earnings for the remainder of this year. As such, I expect average net interest income over the last three quarters of 2021 to remain flat at the first quarter’s level of $24 million.

Existing allowance for loan losses appears excessive

BCB Bancorp’s provisioning expenses are expected to remain subdued in the coming year as loan loss provisioning looks excessive. Allowances accounted for 1.5% of total loans at the end of March. In comparison, the company reported net charge-offs of just $27,000 in the first quarter of 2021, which is 0.005% of average loans on an annualized basis.

In addition, the credit risk of the portfolio appears low as the company no longer has any COVID-19 related credit forbearance as mentioned in the earnings release. Additionally, BCB Bancorp is focused on residential and multi-family loans, which have relatively low credit risk amid the pandemic.

Management mentioned in the earnings announcement that it believes its reserve level is sufficient to cover potential credit losses due to the pandemic. In view of the above factors, releases of credit risk reserves cannot be ruled out in the coming quarters. To be cautious, I don’t expect any major releases this year. Overall, I expect the company to report a provision expense of $3 million in 2021 compared to $9 million in 2020.

Expected full year earnings of $1.66 per share

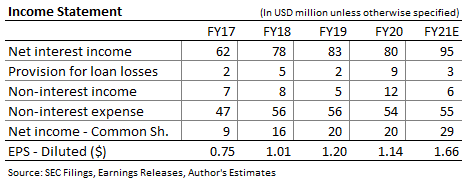

Expected credit growth, revaluation of deposits and decrease in provision costs are likely to boost earnings this year compared to 2020. On the other hand, pressure on average portfolio returns is likely to weigh on earnings growth. Overall, I expect the company to report earnings of $1.27 per share for the final three quarters of 2021, which will bring full-year earnings per share to $1.66, an increase of 47% compared to the previous year. The table below shows my estimates of the income statement.

Actual returns may differ materially from estimates due to the risks and uncertainties related to the COVID-19 pandemic and new variants.

BCBP offers a 4.1% dividend yield

BCB Bancorp offers a high dividend yield of 4.1%, assuming the company maintains its quarterly dividend at current levels of $0.14 per share. BCB Bancorp has maintained this quarterly dividend level since 2014; Therefore, the company is unlikely to change it now.

Earnings and dividend estimates point to a payout ratio of just 34% for 2021, well below the three-year average of 51%. Therefore, there is room for a dividend increase. However, BCB Community Bank’s leverage ratio appears to be somewhat close to the minimum requirement. As mentioned in the 10-Q filing, the bank had a leverage ratio of 10.07% at the end of March 2021. By comparison, the minimum requirement under the FDIC’s Community Bank Leverage Ratio (“CBLR”) will increase to 9.0% in January 2022. Taking these factors into account, I expect the dividend level to remain flat this year.

Target price for December 2021 indicates high upside potential

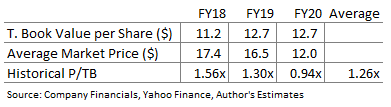

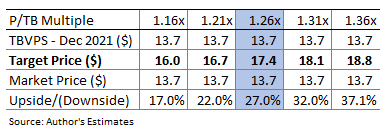

I use the historical multiples of price to nonfiction (“P/TB”) and price to earnings (“P/E”) to value BCB Bancorp at 1.26 in the past as shown below.

Multiplying the average P/TB multiple by the projected tangible book value per share of $13.7 gives a price target of $17.4 by the end of 2021. This price target implies a 27% increase from the June 15 closing price. The table below shows the sensitivity of price target to P/TB ratio.

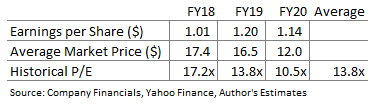

The stock has historically traded at an average P/E of around 13.8x, as shown below.

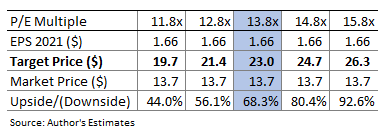

Multiplying the average P/E multiple by the forward earnings per share of $1.66 gives a price target of $23.0 by the end of 2021. This price target implies a 68% increase from the June 15 close. The following table shows the sensitivity of the target price to the P/E ratio.

The same weighting of the price targets from the two evaluation methods results in a combination Price target of $20.2, representing a 48% increase over the current market price. Adding the expected dividend yield gives an expected total return of 52%. Therefore, I assume a bullish rating for BCB Bancorp.

The company’s profits should rise this year thanks to an expected pickup in credit demand in the states of New Jersey and New York. In addition, subdued borrowing costs and the possibility of lower deposit costs should boost returns this year. Additionally, the stock appears to be trading at an attractive level that is a significant discount to the year-end price target.